|

| |

|

| |

|

|

|

|

|

TCHS 4O 2000 [4o's nonsense] alvinny [2] - csq - edchong jenming - joseph - law meepok - mingqi - pea pengkian [2] - qwergopot - woof xinghao - zhengyu HCJC 01S60 [understated sixzero] andy - edwin - jack jiaqi - peter - rex serena SAF 21SA khenghui - jiaming - jinrui [2] ritchie - vicknesh - zhenhao Others Lwei [2] - shaowei - website links - Alien Loves Predator BloggerSG Cute Overload! Cyanide and Happiness Daily Bunny Hamleto Hattrick Magic: The Gathering The Onion The Order of the Stick Perry Bible Fellowship PvP Online Soccernet Sluggy Freelance The Students' Sketchpad Talk Rock Talking Cock.com Tom the Dancing Bug Wikipedia Wulffmorgenthaler |

|

bert's blog v1.21 Powered by glolg Programmed with Perl 5.6.1 on Apache/1.3.27 (Red Hat Linux) best viewed at 1024 x 768 resolution on Internet Explorer 6.0+ or Mozilla Firefox 1.5+ entry views: 2760 today's page views: 473 (23 mobile) all-time page views: 3832826 most viewed entry: 18739 views most commented entry: 14 comments number of entries: 1279 page created Wed Jul 22, 2026 01:54:40 |

|

- tagcloud - academics [70] art [8] changelog [49] current events [36] cute stuff [12] gaming [11] music [8] outings [16] philosophy [10] poetry [4] programming [15] rants [5] reviews [8] sport [37] travel [19] work [3] miscellaneous [75] |

|

- category tags - academics art changelog current events cute stuff gaming miscellaneous music outings philosophy poetry programming rants reviews sport travel work tags in total: 386 |

| ||

|

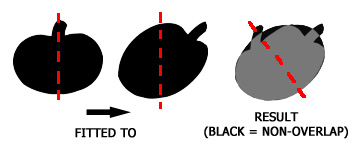

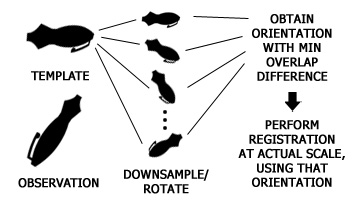

- Al Warden, Apollo 15 command module pilot, man after my own heart Had a first this week when I got a call from a financial advisor on the lab phone (the number which, I confess, I do not myself know). Since I have definitely never written it on any form, I can only conclude that he got it from the university directory or somesuch. Well, in the face of such enterprise and industry, I ain't even mad. It was with some amusement that I read about several verses of the Army staple Purple Light being blackballed, thanks to action from AWARE. Personally, while I wasn't particularly enthusiastic about those lines back in the day, I'm still not too supportive of the complaint; in any case, one realises that AWARE seem to have no problem at all with the new boyfriend being killed (which they more or less acknowledge), and if we start sanitising all the lyrics, where would that leave us? Here, a good Professor of Law's retort to the sisterhood trying to ban lad mags rings particularly true. Anyway, if I know the Army, the song's simply going to enjoy a resurgence, with all-new yet oddly similar lyrics, on those hot sweaty nights in the jungles of Tekong. Not that I ever figured out what the purple light actually referred to. Purple waterfalls, though... Unanimous Winner - Minister for Social and Family Development on poverty [N.B. There is errata on the initial analysis on poverty; the situation is likely less dire than initially feared, but the main points still stand. Refer to the updated post for details] Three weeks after the poverty line debate, in which it was noted that any reasonable definition (subject to more deliberation here) would have 20% of locals classed as poor (note that the average figure from multiple past studies, from a recent SMU-Lien Centre report, is about 19%*, so it shouldn't be too far off), and a week after the income distribution could not be deduced, the last word is apparently that nothing relevant will be revealed, but everything will be said. Capping it all off is the obligatory homely analogy, with kueh lapis following in the grand tradition of XO Sauce chye tow kuay, mee siam mai hum, rojak society and Sampan 2.0. Reading further into it, it can be noted that kueh lapis layers are extra thin to begin with. While the Minister does make the good point that fixing a line as a percentage of the median is not extremely meaningful (nothing stopping him from using a cost-of-living approach, though), and that multiple lines are better, it is then glaring that still no hard numbers are given. Okay, you say many lines good, so draw those lines lah - how many are sibei jialat, jin gan kor, tan buey gao? I see nothing that would prompt me to withdraw my original assessment. [*Parliament did have a passing mention last year on the Average Household Expenditure on Basic Needs (AHEBN) for a four-member household being S$1250, not far from the bare-bones S$300 per person that I calculated, but further without accounting for transport, and including CPF. Talk about theoretical assumptions...] Well, it seems like the end of the story, with the final final word being that, in the quite improbable case that there are actually poor people here (got meh), they aren't (openly) dying of exposure or starvation, so we don't even have to estimate how many of them there are. So what if advanced nations like Switzerland, Sweden, Japan etc all maintain one? Case closed. Job well done, pat on back. Punggol II, 6.9 million, here we come! And In Our Schools Meanwhile, schools here shrugged off another attack by a resurrected Messiah (as was hinted at), as they came under the spell of the all-important release of PSLE results, this time without even mentioning the top score (which was 285 last year). This move turned out to be kind of useless in actuality, because any slightly-resourceful concerned parent* would just hop over to KiasuParents or similar forums to get a pretty good approximation; with the maximums from about half the schools already published, the current best known result is 275 from perennial frontrunners Raffles Girls', and the five-point drop in the Edusave Entrance Scholarships cutoff seems to indicate that the range has indeed become narrower. Said resourceful parents are, of course, not swallowing the "all schools are good schools" line at all (as Herr Ahm prophesied), with 92% (of 117) disagreeing on the forum thread. Lest it be said that they're just nameless noises, the vice principal of Jurong West Secondary School finally openly gave voice to the unspeakable: "How many of our leaders and top officers who say that every school is a good school put their children in ordinary schools near their home? Only until they actually do so are parents going to buy it." Going back into Herr Ahm claiming that the connection between a top secondary school and a degree is strong, some qualitative statistics have been well-illustrated. For example, it happens that 60% of primary school GEP kids and 50% of Integrated Programme students live in non-HDB property, compared to only 20% of the population at large. There are two main lines along which this can be explained. First is that these kids got better tuition and other support because they were richer, and thereby qualified for exclusive education. The other is that they got in because they were inherently smarter (or at least more academically-inclined), a trait they partly inherited from their parents, who in turn are richer due to themselves being smart. Personally, both factors have an influence, and therefore the concern should be that the balance seems to be shifting towards the former. Myself, I'm just waiting for the PSLE banding committee to be announced, so as to hear what they have to say. [*Not a shade on my grandma's info-gathering network, fondly dubbed Her Majesty's Secret Service in its heyday] Round, Round - Some of the best advice on learning that I've ever read Congrats, you have now mastered waveforms! Still, while that may be true, the process still ain't easy. Often, while one gets the big picture well enough, there remains a huge amount of mind-numbing nitty-gritty to be done, to translate concept into practice - many people can "get" gravity with rubber sheets and heavy balls, but how many of those can calculate the motions of astronomical bodies? Applied to Friday's presentation by a visiting professor on image registration, my layperson explanation would be that to morph shape A into shape B, both shapes are "coloured" by the same rule to get an idea (see page 3 of the paper). Many different such rules are then applied, and some sort of average is used to produce the eventual transformation. The nice part is, no pairs of matching points need be defined, and the results are far better than texture-based methods such as from SIFT on simple images like traffic signs (see 6.3.1; identification, though, might be achieved well by neural networks). It can however be noted that in most of the examples, the rotation applied is not particularly large, and therefore naïvely speaking the integral area, along most axes, should be similar under such distortions. However, it's not that good when key features are misaligned, such as the apple stem in Figure 4:  The stem in the template apparently got mapped to the smaller left peak. I suppose using copies at multiple rotational orientations might help to alleviate cases such as these, and where the observation differs from the template by more than say 45 degrees. Indeed, the paper does warn that the method is not particularly good with occlusion, or any noise that results in uneven errors. Well, to cover arbitrary rotations, a downsample-rotate (DoRo) fitting step might be enough, exploiting the robustness-at-even-subsampling property.  Then again, I might have completely misunderstood how the method works, and if so, my apologies Nice thing is, experiments on this can be done using the nonlinear fitting step as a black box, and personally I expect it to offer rather improved correspondences at large rotational divergences (making for some impressive-looking figures), with not too much additional time taken. Of course, there are practical implications when the observations can indeed be highly rotated, which is not really the case for the street signs and medical images that the paper used, but plausible in other domains (e.g. objects emerging from a conveyor belt). Could make a cute technical report for somebody. That said, fairly impressive results were obtained on MNIST (it would have been interesting had an all-against-all matching been performed as a classifier, with say ten representative training examples from each class from the training set - a couple of weeks would be needed, though) To me, the most interesting part was the "affine puzzle" bit on realigned deformed fragments without correspondences (42 minutes into the video), which is suggested can also be cast as a system of equations. That led me to wonder if it can be extended to work efficiently with a larger library of fragments (many of which may not appear in any given template) instead (now what problem does that sound like?) All in all, this looks like a good contender for registration whenever orientation can be roughly accounted for, and speed of computation appreciated (but then, when is it not?) Recruitment And Reviews Before I begin, I would like to define a few abbreviations:

So, this Thursday morning, I got an email that J.P. Morgan was holding a recruitment talk for quantitative researchers (i.e. quants) that afternoon. Seeing as I had just happened to have borrowed a few books (those above) touching the area, and happened to meet their requirement of being a postgrad student in a math, (financial) engineering, physics or computer science, I figured that I might as well pop over for a listen. The presentation, with some commentary, follows. The guys who are doing an MFE might find it informative. To start off, have a guess at how many quants there are at J.P. Morgan (which seems to be the current top investment bank by fees earned). Perhaps unsurprisingly given that most of the hundred or so attendees were from the PRC, it was asked why the quant centre for China was in Beijing and not Shanghai, given that the latter is the country's financial heartbeat. The answer was that it was due to Beijing having a much bigger pool of candidates, what with all the premier universities situated there, though it was admitted that they hadn't actually started doing any local business yet. One could however suspect that it's partly down to there being where the real power lies... But what do the quants actually do? Well, about half of them support market-making business, particularly in derivatives pricing; they create hedging strategies, price quotes, manage portfolio risk and perform risk analysis, with some algorithmic trading thrown in (this doesn't appear to be their speciality, though, and from what I gather their involvement is mainly defensive, to not get ripped off by others). The other half support risk management and finance (alright, so the distinction with the above isn't that obvious). This involves calculating counterparty exposure and maintaining credit risk engines, developing capital, mortgage and benchmarking models, and also reviewing and validating said models. The (work/infomation) flow was presented in this order:

With the bolded areas where the quants come in. Digression number one. The appearance of VaR (value at risk) caught my eye, with The Number That Killed Us (TNTKU) devoted to disparaging this single metric. The book begins with Taleb wearing a tie to address the House Committee on Science and Technology in 2009, on this very VaR. Basically, Taleb says, VaR is condemned to be a hopelessly useless estimate of risk, since it is calculated using past behaviour, and the theory rests on upcoming risk mirroring the history of the asset, using normality (Gaussian) assumptions, and moreover over an arbitrary length of time. [N.B. The presenter, who has a background in physics, did point out in the Q&A that one of the big differences between finance and physics is that the former is not replicable] Coincidentally, it happened to be J.P. Morgan who gave VaR to the world in 1994, five years after its conception, as part of RiskMetrics, and it was soon adopted by other major players. This helped to convince the Securities and Exchange Commission that the banks had found the silver bullet to tame risk exposures once and for all. Triana doesn't have a particularly high opinion of quants (referring to them as QuAnts throughout), and points out that while regulators did retain VaR, they probably did so to avoid uncomfortable questions about why they allowed it in the first place, they are now demanding a stressed value at risk (sVaR) addition, where the data used is the most volatile possible for each asset, as well as an Incremental Risk Charge. Naturally, since the banks still get to calculate those figures for themselves, Triana doesn't think those measures will work out. He then accuses QuAnts of being like engineers who build weapons of mass destruction and then disavow their misuse, only less honest about their intentions. Supposedly, Raymond May, its inventor, saw it only as a gauge of relative risk, but that didn't stop it from getting freaking big. Let's zoom out a bit here. VaR is hardly the only model that got heavy stick for spitting out a single quantifier - recall the Gaussian copula thingamajic (again by a J.P. Morgan employee) discussed three years back, with the prediction that the next bust would be due to the Student's t-distribution Pancake Pizza function? Why did both explode so badly? I'll first go into why, and then into why they didn't. Give Me A Lever  And I will move the world (Source: consciousmind.org) Both VaR and the Gaussian copula wound out to have severely underestimated possible risk. But on the flip side, if you underestimate risk, you are justified in taking more risk, often by increasing leverage; and when you increase leverage, when things go well, you make more profits. Double leverage, double profits (or more, given fixed initial and transaction fees), get a fancier job title and more money to manage. Gee, is that enough incentive to tilt financial institutions towards underestimating risks, I wonder? Now, as to why the models worked as they should have. It really depends on what one thinks that the models are supposed to do. Protect the world economy? Reduce market inefficiencies for the common good? Nah, how about "line the pockets of banksters (and quants)"? Now we're getting somewhere. I propose the Four Axioms Of Guaranteed Market Crises:

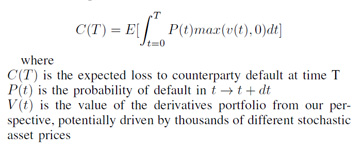

If these hold true, periodic malfunctions are inevitable. The cycle is as follows: right after the last crash, with the populace yelling for bankers to be hung from lampposts, then drawn and quartered before being burnt and stomped on, both regulators and banks prostrate themselves and swear to abide by extremely strict rules on taking risks, and indeed there is a credit squeeze as the banks simply refuse to lend money. However, they are probably now overestimating the true risks (whatever those may be), and slowly the braver financiers begin to peek out of their shells. Their slightly more adventurous bets and loans pay off safely. They get promoted. Others follow suit. Conservative sticks-in-the-mud are squeezed out for their relatively poor returns. In a few years, all is forgotten. They start to wonder why they should be happy with 10x leverage, when the firm of J.R. Arbuckle down the street is raking in ten times that with their 100x leverage, and their coffee boys are zipping about in new Jaguars. Industry-wide, risk and leverage ratios creep up. sVaR schmar, if we use only data from the last six months, and ignore those two completely unfortunate losses by the overseas subsidiary - those don't count, right? - and average the returns with other, similar companies, the risk is now acceptable! The figures say so, the model has okayed it! Dear reader, what do you think happens soon? [N.B. I was deliberating whether to ask about their opinion on VaR, its historical failings and the validity of my Four Axioms in the question-and-answer session, but ultimately resisted as I thought it unproductively pointed] Anyway, the take-home is that nobody actually knows the risks. The quants don't, but Taleb and other critics don't either. But the risks still exist, so if life is to go on, the only choice is between placing their determination in the hands of a bunch of number theory and quantum physics Ph.Ds, or a smoky backroom of old-school alpha male bankers. Clearly, neither option is foolproof, but it's not like markets didn't sink into excess or crash before all that fancy math, just that nowdays, the crash tends to be in a slightly more rigorous fashion. Note also that it's hardly only the banks' fault - disregarding the true risk, if Bank Garang comes up with lower estimates than Bank Humji for any reason at all, whether by a million-parameter model or because their CEO had a good feeling about it, and are therefore able to deliver higher returns, over time who will both institutional and individual clients flock to? Strategy Versus Tactics On to Barbarians At The Gate (BATG), which details the fate of RJR Nabisco, and the largest leveraged buyout in history. It is impossible to read it after TNTKS without getting the impression that, although both books describe finance, their subjects inhabit totally different worlds. The history of R.J. Reynolds was a classic American riches-to-unthinkable-riches story: son of prosperous tobacco farmer builds huge cigarette empire, becomes hometown hero, his good ol' boy employees get wealthy, doing hard, honest work. This happy state of affairs persisted for most of a century, and while I gather that the workers of Winston-Salem would not have thought of themselves as sophisticated, but hey, did cigarettes sell. This everyone-knows-everyone, promote-from-within culture couldn't quite last, and outside management was recruited in the face of competition from Philip Morris. Even then, though, one never gets the idea that they knew much advanced calculus either. Oh, there's a ton written about politics and personality - who brought who on the board, who likes to splurge on luxuries for his office, whose wives got along, who hates whose guts - but precious little calculation. The closest we get in this respect is the 30 year-old Kohlberg Kravis Roberts analyst Scott Stuart, who was tasked with assembling projections for the company's cash flow, and he was stymied by uncooperative managers. The major players were almost without exception "big picture" guys who disliked "Wall Street gobbledygook", insisted on talking man-to-man without lawyers, and mostly decided on bid amounts before figuring out if they could come up with the money. A representative example of this attitude surfaces towards the end, when a party that had already nearly exhausted themselves with a US$108 per share bid, up from an initial valuation of about US$75, threw in an extra fifty cents, or US$115 million in total, because some young associate said that "they had come too far not to win it", just like that. Certainly, a long way from solving hundreds of simultaneous equations to get the optimal price point; if most quants are tacticians, those movers-and-shakers are strategists. There's more of a mix in More Money Than God, with some hedge fund pioneers straddling the two. Bruce Kovner, for instance, was described as delegating assistants to track numbers, and then milked the carry trade for years before others caught on. Interestingly, George Soros' side of the story for his part in the Thai currency crisis of 1997 is given: apparently, he believed that he was a virtuous speculator who was alerting the Thai government that the baht had to devalue, and that by preventing them from procrastinating, the eventual impact would be cushioned; his making US$750 million out of it was mostly incidental. Definitely not tactics. Then we have the oddballs from The Big Short, about the few who saw through the subprime crisis: "John Paulson was oddly interested in betting against dodgy loans, and oddly persuasive in talking others into doing it with him. Mike Burry was odd in his desire to remain insulated from public opinion, and even direct human contact, and to focus instead on hard data and the incentives that guide future human financial behviour. Steve Eisman was odd in his conviction that the leveraging of middle-class America was a corrupt and corrupting event...". It takes all sorts. Not that it's easy being a tactician. Just to give a taste of what one would be in for, the presenter had slides on how partial differential equations were used to solve the Heston stochastic volatility model for foreign exchange knockout options. Next up was algorithmic equity order execution, or finding the optimal trajectory of buying stock as to minimize total cost. Intuitively, buy too fast, and you might shift the market to your detriment; too slow, and you risk not completing your order book in time (again, of course, the order itself is strategy - this squeezing cents out of it is tactics) Finally, we come to counterparty credit risk, where the maximum loss is estimated:  Well, ok, it's just a big huge massive Monte Carlo simulation. That sort of thing I can do (I think). Pointedly, in the Q&A, a quant revealed that his most satisfying moment was building a model that handled four levels of options, i.e. derivatives of derivatives of derivatives of derivatives. I can't imagine how pleased Buffett (perhaps the ultimate strategist) must be... Finally, according to them, they have begun to move away from pure theory, which was all the rage a decade ago - might a little strategy have been delegated down the ranks, as has become popular in militaries? They do also admit that commodities models are more ad-hoc, which makes sense since with fewer market participants, the quirks of individual competitors matter a lot more. [N.B. When coming across Clausewitz writing "Everything in war is very simple but the simplest thing is difficult", I could not help but recall Moravec's paradox, which can be paraphrased as "In artificial intelligence, the hard problems are easy and the easy problems are hard". Things do interconnect a lot] If there's one thing I took from the talk, it would be that if I ever seek a job in this field, and am asked why I want it, I will answer: "The money and the challenge". I mean, what do I say, my life's ambition is to create efficient markets for the betterment of mankind? What am I, a Miss Universe hopeful? Oh, one thing - apparently, when applying to be a quant, the application goes directly to the quants, and not through HR. That's something. Next: Pieces And Bits

Trackback by billig parajumper

Trackback by parajumpers blazer

Trackback by canada goose storlekar

Trackback by canada goose mystique parka

Trackback by download cs go hacks

Trackback by battle camp hack tool

Trackback by google plus app for blackberry

Trackback by Steam Wallet Hack

Trackback by review affiliate course internet marketing

Trackback by Hay Day Cheats Free

Trackback by best dating sites

|

||||||||||||||||||||||||||||||

Copyright © 2006-2026 GLYS. All Rights Reserved. |

||||||||||||||||||||||||||||||